A bit off topic, but I just can’t resist blogging about any useless or counterproductive federal agency.

A couple weeks ago, my gym membership dues hit one of my debit cards and overdrafted one of my checking accounts (the perils of having more than one account, it seems, is that occasionally one ends up empty… but I digress…). This shocked me, since federal rules that went into effect in 2010 bar debit overdrafting and associated fees without an explicit opt-in, which there’s not a chance I would give. I called my bank and asked if they enjoyed flouting federal rules, to which they replied that these rules only apply to “one-time” transactions and my gym membership doesn’t count.

A quick review of the rules shows that they are correct that these rules apply only to “one-time” transactions, but there’s no definition of “one-time.” Debit card transactions aren’t “scheduled” with the banks or anything — merchants process them as agreed whenever they get around to it, so really, every transaction, in my opinion, is “one-time.” So where is the line drawn? If I go to a restaurant twice and use the same card, is that no longer one-time? Does it have to be on regular intervals or a specific number of instances?

The agency responsible for the rule gets the first pass at defining the ambiguous (that is, courts give “deference” to an agency as to the interpretation of their own rules, so long as that interpretation isn’t absurd). So I asked the agency responsbile for the rule: while original the rule was issued by the Federal Reserve, authority for the rule was passed on to the Consumer Finance Protection Bureau upon its creation in 2011. So I e-mailed the agency asking for their interpretation of “one-time,” and was surprised to get a fast response from an attorney for the agency who asked me to call him to discuss. I politely declined, explaining that I’d prefer it by e-mail such that I could forward a copy on to my bank if the interpretation was useful for the return of my $35 overdraft fee.

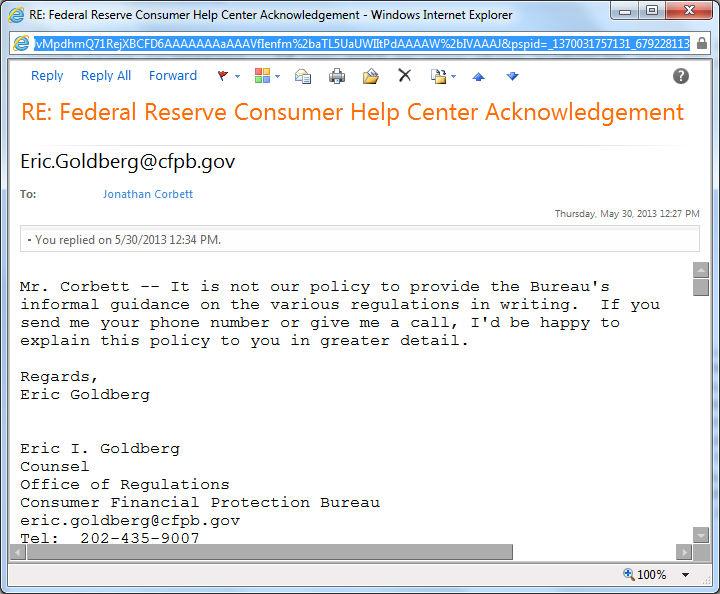

Here’s where it gets weird (well, weirder than a government agency that’s actually responsive other than when they want your money): The CFPB attorney refused to tell me the agency’s interpretation in writing. At first I’m told that “informal” guidance can’t be given in writing, and upon asking how to get formal guidance, I was told that individuals can’t.

Here’s where it gets weird (well, weirder than a government agency that’s actually responsive other than when they want your money): The CFPB attorney refused to tell me the agency’s interpretation in writing. At first I’m told that “informal” guidance can’t be given in writing, and upon asking how to get formal guidance, I was told that individuals can’t.

So if consumers can’t get informal guidance in writing or formal guidance at all, who is this “Consumer” Finance “Protection” Bureau protecting? Is this another one of those, “we’ll protect the people by protecting the financial institutions” type things? Too big to fail, too big to jail, and too big to talk about in writing (unless, of course, they request it). Naturally, they picked the wrong person to refuse — I’ll be continuing my query via Freedom of Information Act requests until I have my answer.

Stay tuned tomorrow for the start of our 30-part series, “No Surveillance State Month,” where daily for the month of June I’ll be posting ways to avoid invasion of your privacy in the digital age.

I work with bankers on a daily basis-they do NOT like the CFPB at all. If anyone has trouble getting credit in the future-it is their fault not the banks. They are restricting things so much “for our own good” that they are making financing hard to get. I read an article recently on allegedly the CFBP is keeping/tracking our personal info/credit card use. Someone sent me this link: http://cfpbspotlight.com/petition/

Also out of the two big too fail..BASEL III is going to make it more expensive or harder to get home loans more than 80% LTV or HELOCs because of govt over reach and over regulation.

Perhaps they exist merely to piss of everyone, then. 😉

I appreciate the hard work you put into checking the unbridled authority of the TSA and other government over-reachers. But I’ve been reading your material for some time now, and I hope you are willing to accept some constructive criticism.

I’ve read your legal briefs, which while quite articulate, have a constant edgy thread in them of sarcastic remarks that really have no place in civil discourse, especially where a judge is being addressed. In this blog post you do something similar, with the sarcastic comment “I called my bank and asked if they enjoyed flouting federal rules…”

Perhaps you didn’t really use that language with your bank, but even if you didn’t, it’s rude and impolite to imply that whatever problem your experiencing is the fault of the person you’re addressing (which is what the above remark does). It also degrades public discourse when you weave sarcasm into documents that are part of a legal process that, for good or bad, is the best we’ve got.

Feel free to ignore my advice. But as someone who’s been around the block and is twice your age, I can tell you that the age-old adage “you catch more flies with honey than vinegar” is dead on correct. Please consider toning down the sarcasm in your future interactions with others.

If your language were only affecting you, I’d be less inclined to make this suggestion. But it is affecting all of us who interact with the government through the legal process. You give the adversary ready cause to discount your, and our, arguments as the ravings of eccentrics.

There are lawyers who are really good at leaving emotion out of legal briefs. There are lawyers who try to use passion and emotion in order to convey that point. Successful and unsuccessful types exist in each bunch.

You see, when I’m writing about the TSA, it’s a geuninely emotional topic for me. I receive thousands of e-mails, comments, and occasionally even phone calls from people who have been abused by the TSA, and I’ve been abused by the TSA myself. With that being the case, when I’m replying to a government argument that, for example, I shouldn’t have any right to present evidence, I’m not emotionless, and I don’t think letting that fact show through in my legal writing hurts my case. You may catch more flies with honey than vinegar, but I’m sure your generation also has a saying about how being genuine is admired and respected.

Finally, every once in while I get advice that comes tagged with a note that doing otherwise will hurt the cause, set bad precident, make things more difficult, etc. But, the fact of the matter is that legally, I represent only myself when I fight the TSA, and I have the right to do that in a manner dictated solely by my own discretion and guided by my personal interests. I am very happy (thrilled, even) that my work helps the community to hold onto its rights and might do some good for the world. That certianly motivates me. But in the end, if the community (or any member thereof) thinks I’m not doing a good job, or that my filings don’t represent what others want, the community is free to file its own lawsuits, get its own precident set, run its own protests, and petition its own grievances. I feel that the fact that only a handful of the 300+ million American people have filed suit against the TSA implies that they feel that their rights are being adequately represented in court already.

I do appreciate your feedback.

–Jon